May 11, 2026: City Council meeting agenda

- 9A: Review and consideration of a summary overview of the findings of the Resident Budget Task Force (COUNCIL).

- 9B: Review and consideration of the Fiscal Year 2026-27 Preliminary Combined Financial Program for the City of Cerritos and the Successor Agency to the Cerritos Redevelopment Agency (COUNCIL/SUCCESSOR AGENCY).

May 5, 2026: City Council meeting agenda for May 11 published

- 9A: Review and consideration of a summary overview of the findings of the Resident Budget Task Force (COUNCIL).

- 9B: Review and consideration of the Fiscal Year 2026-27 Preliminary Combined Financial Program for the City of Cerritos and the Successor Agency to the Cerritos Redevelopment Agency (COUNCIL/SUCCESSOR AGENCY).

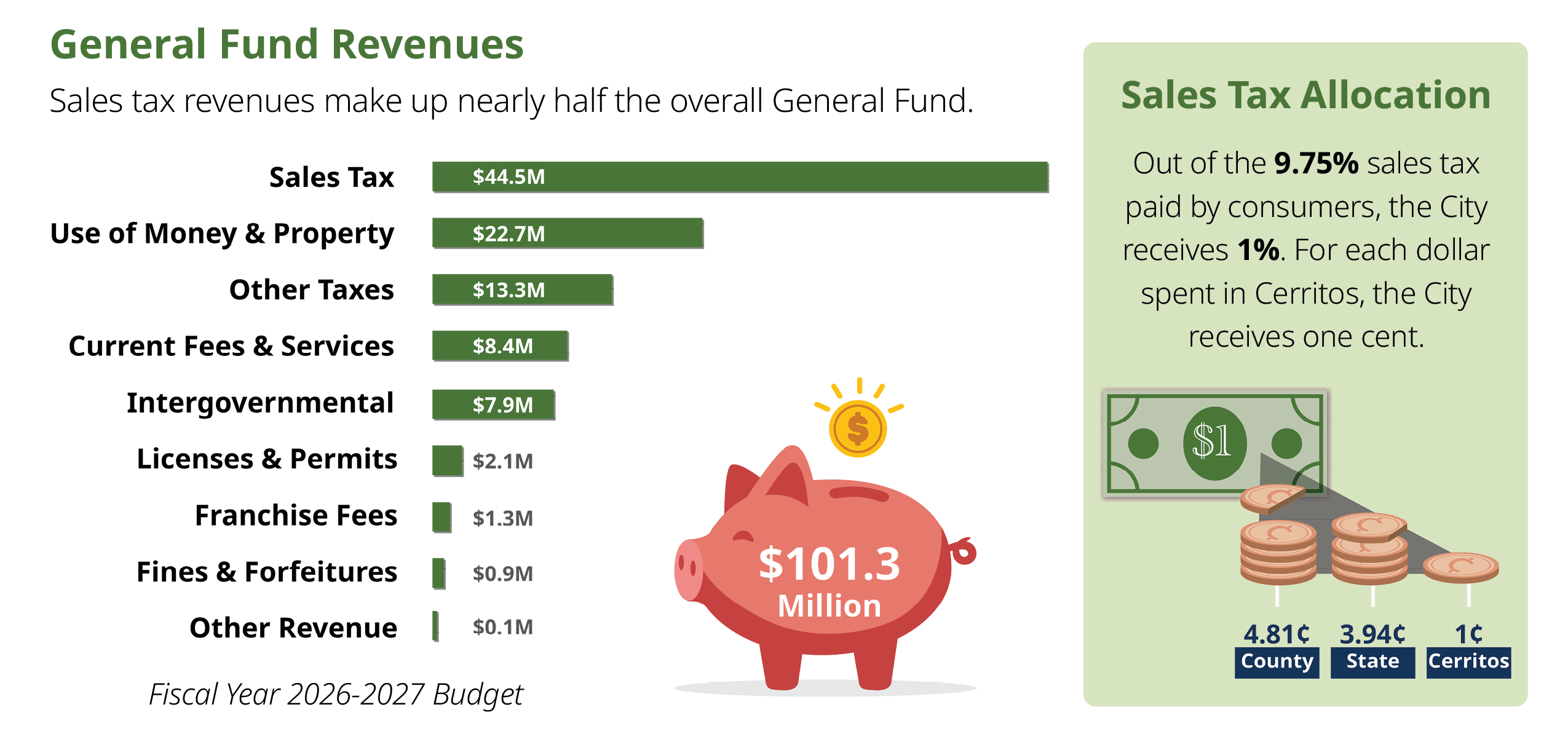

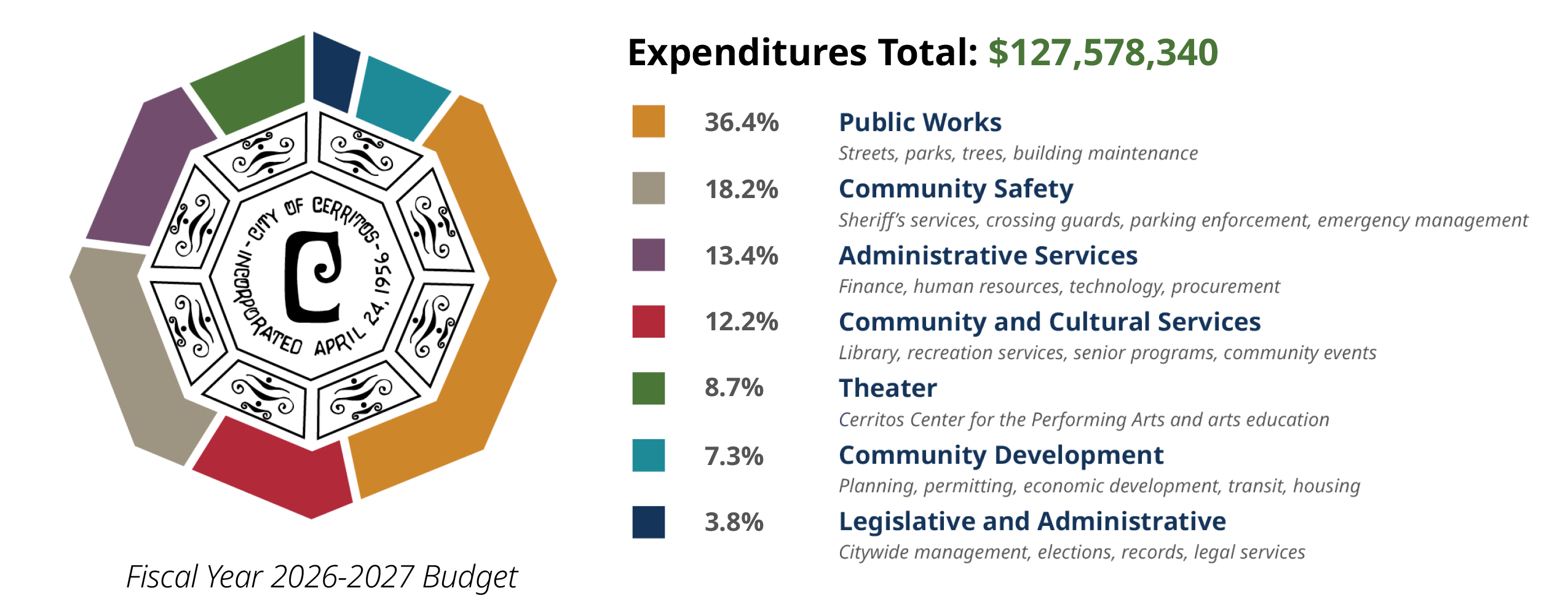

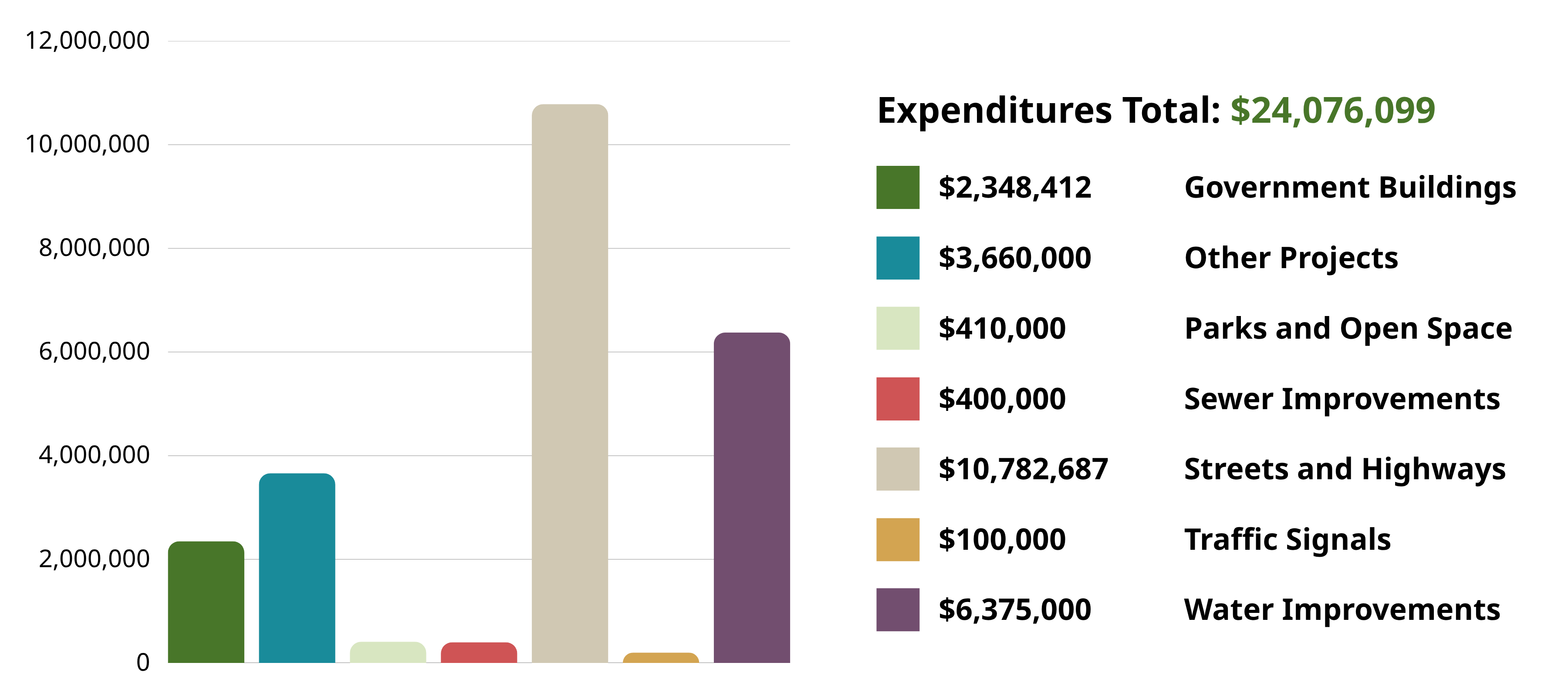

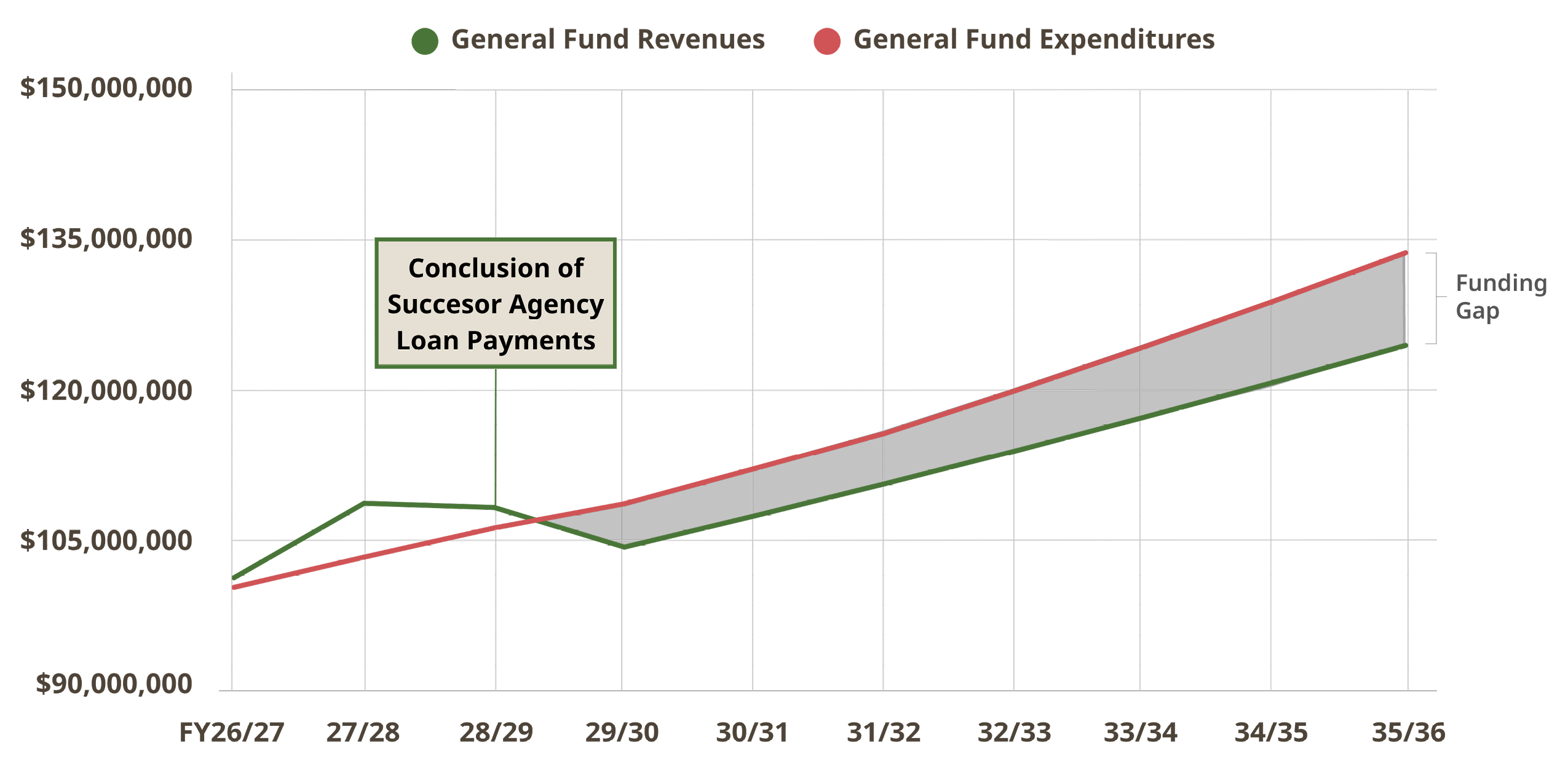

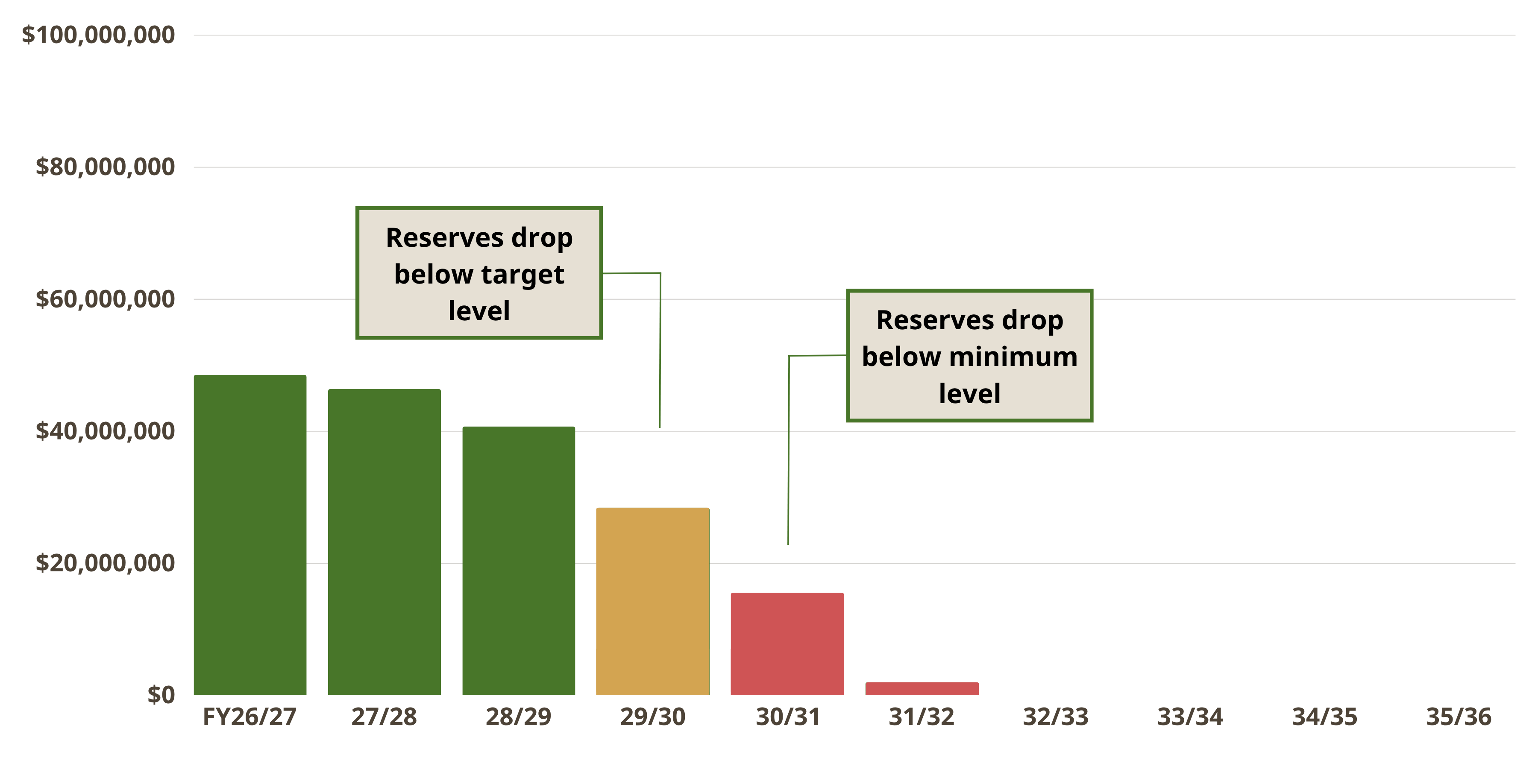

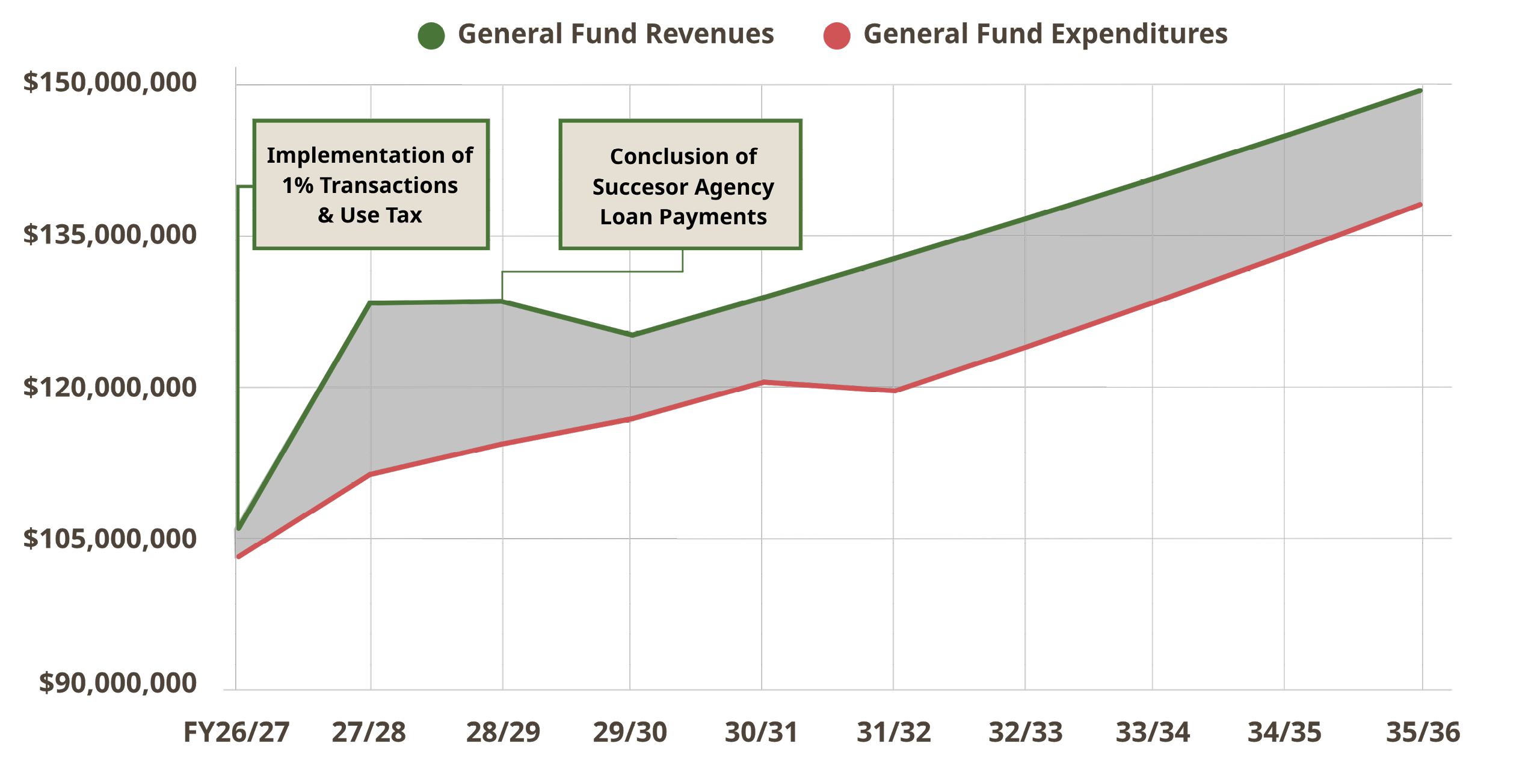

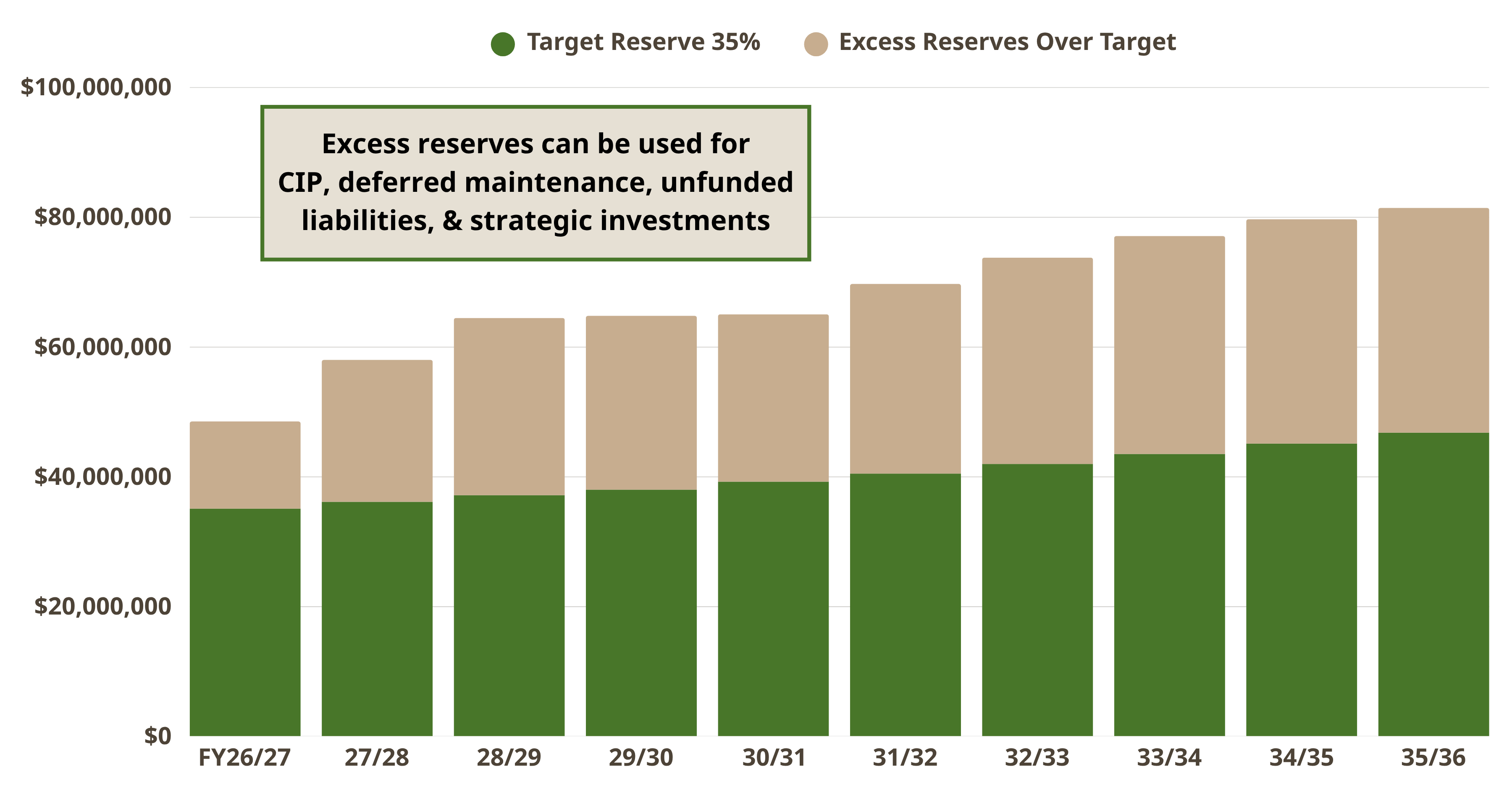

May 1, 2026: Preliminary FY26-27 Budget Book

- The Preliminary City of Cerritos Combined Financial Program for 2026-2027 was published to the City's website.

April 21, 2026: Virtual Community Budget Workshop

- Cerritos residents attended a virtual Budget Workshop

April 15, 2026: Community Budget Workshop

- Cerritos residents attended a Budget Workshop in the Cerritos Senior Center.

April 3, 2026: Budget meeting mailers

- Cerritos residents and businesses began receiving postcards in the mail inviting them to participate in upcoming community budget meetings.

March 9, 2026: City Council meeting

- 9B: Review and consideration of the City of Cerritos Annual Comprehensive Financial Report for Fiscal Year 2024-25.

- 9C: Review and Consideration of the Fiscal Year 2025-2026 Midyear budget update and proposed Fiscal Year 2025-2026 Budget amendments.

December 11, 2025: City Council meeting

- 9A: Review and consideration of information related to the FY 2026-2027 budget development process and Strategic Plan update (Budget Study Session #1)

December 2025: Budget at a Glance mailed

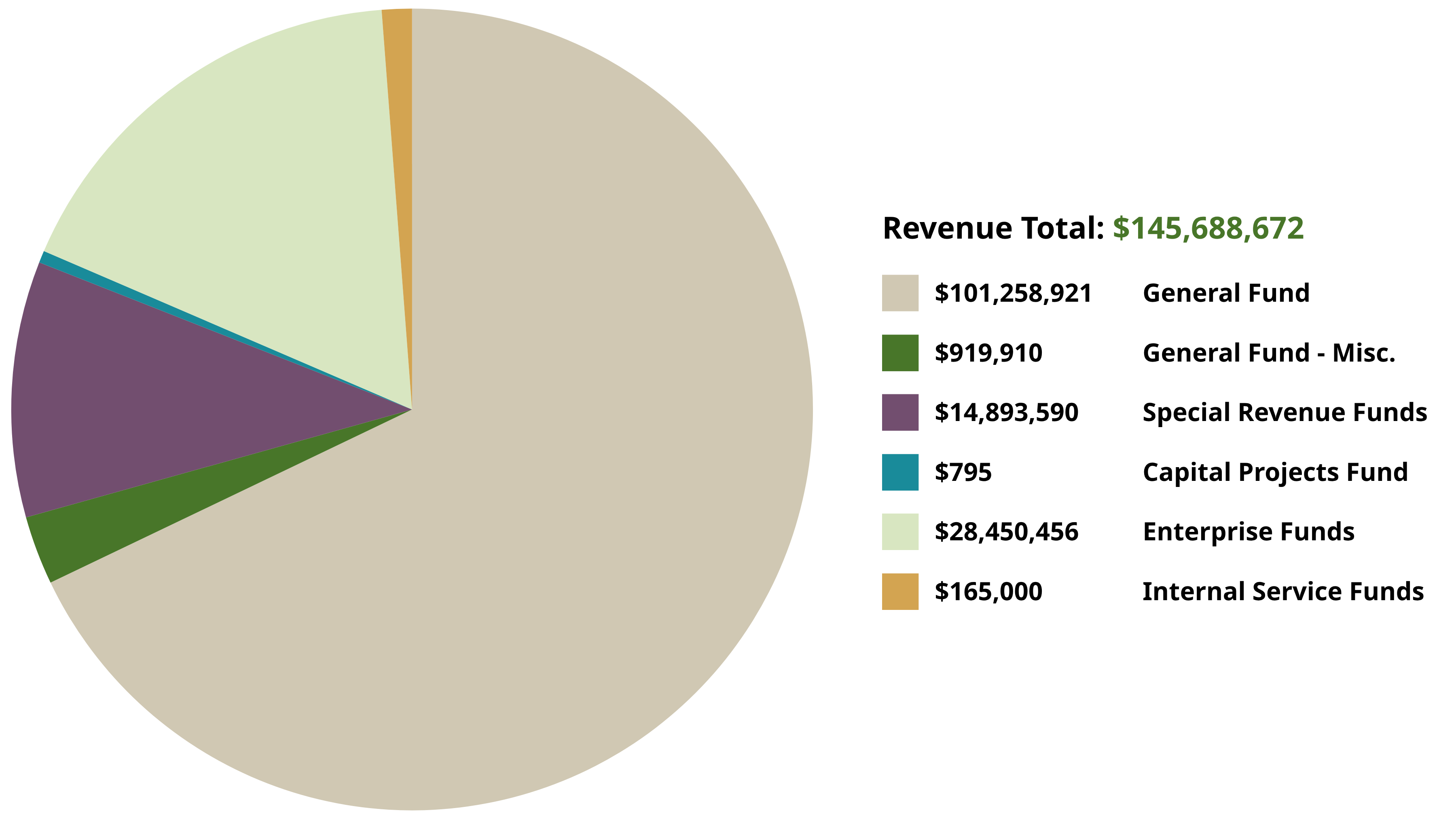

- A Budget at a Glance document was mailed to Cerritos residents in December 2025 to provide clarity on projected Citywide expenses and revenues for Fiscal Year 2025-2026.